Insurance is a vital aspect of financial planning, providing individuals and businesses with the peace of mind that comes from protection against unforeseen events. Understanding the various types of insurance available, from life and health to property and liability, is crucial for making informed decisions that safeguard your assets and future. Each type serves a distinct purpose, reflecting the diverse needs of different individuals and circumstances.

This comprehensive overview will delve into the core elements of insurance, including the intricacies of policies, the factors influencing premiums, and the essential claims process. By evaluating these components, readers will gain valuable insights into how to select the right coverage tailored to their specific needs, ensuring optimal protection and financial security.

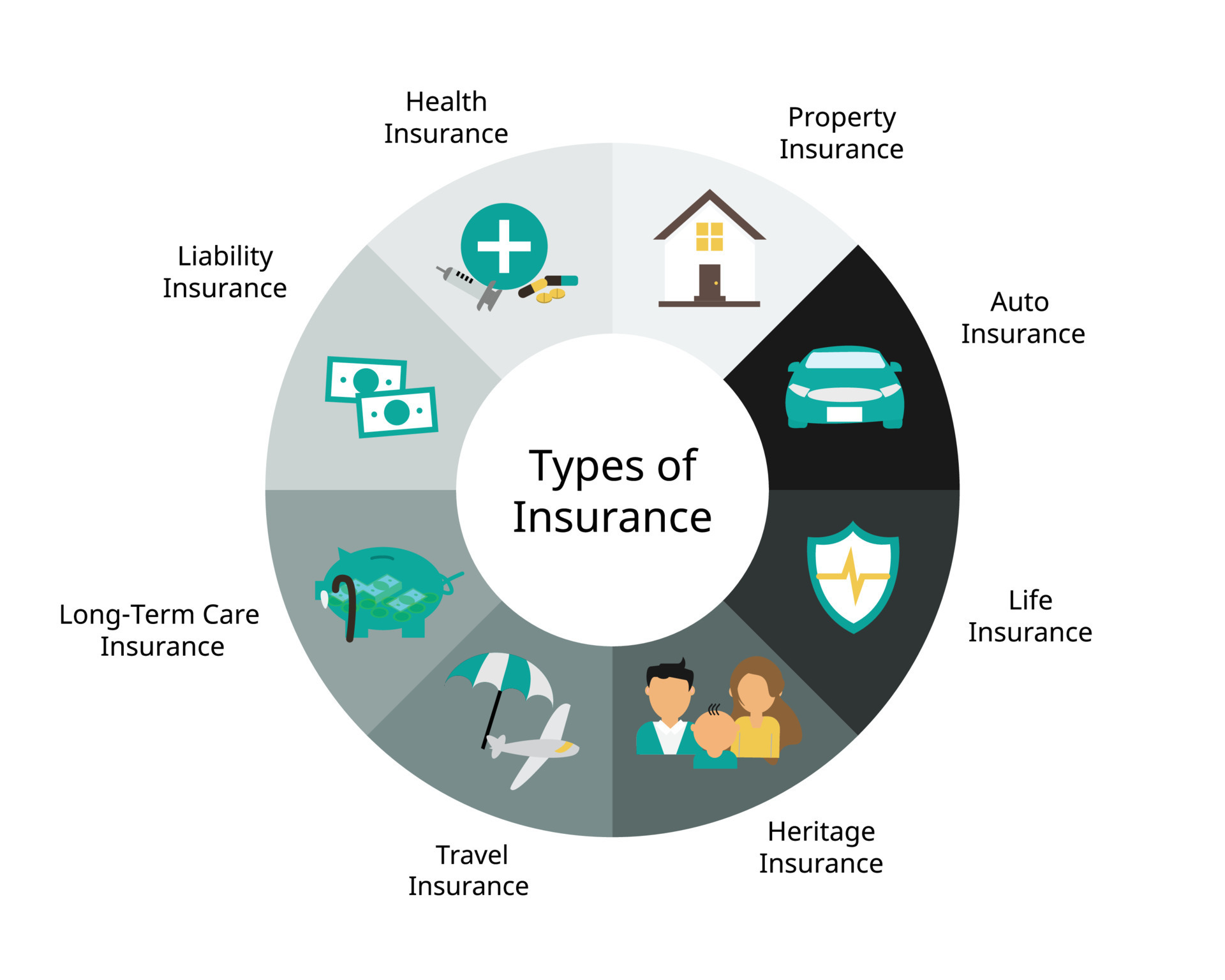

Types of Insurance

Insurance serves as a vital component in financial planning, providing a safety net against unforeseen events. Understanding the various types of insurance available can help individuals and businesses select the right coverage tailored to their specific needs. This exploration of insurance types will clarify how each functions and the importance of selecting the most appropriate options.Health Insurance

Health insurance is designed to cover medical expenses incurred by the insured. It can include a range of services from routine check-ups to major surgeries. For instance, an individual with health insurance may only pay a small co-payment for a doctor’s visit, while the insurance covers the majority of the costs. The significance of health insurance is underscored by its ability to safeguard individuals from high medical bills, thereby ensuring access to necessary healthcare services.Life Insurance

Life insurance provides financial protection to beneficiaries in the event of the policyholder's death. Policies typically pay out a predetermined sum to the designated beneficiaries, which can help cover living expenses, debts, or even educational costs. For example, a parent with a life insurance policy can ensure that their children are financially supported in their absence. Choosing the right type of life insurance, whether term or whole life, is crucial as it directly impacts the financial security of loved ones.Auto Insurance

Auto insurance protects vehicle owners against financial loss in the event of accidents or theft. It typically covers damages to the vehicle, medical expenses, and liability for injuries or damage caused to others. For instance, if a person is involved in a car accident, their auto insurance can cover the repair costs and medical bills for all parties involved. Having adequate auto insurance is essential not only for legal compliance but also for providing peace of mind while driving.Homeowners Insurance

Homeowners insurance offers protection against damage to one's home and personal property, as well as liability for injuries occurring on the property. For example, if a tree falls on a house during a storm, homeowners insurance can cover repairs. This type of insurance is particularly important for safeguarding one of the most significant investments individuals make— their homes—against unexpected disasters.Disability Insurance

Disability insurance provides income protection in the event that an individual is unable to work due to illness or injury. It helps replace a portion of lost wages, ensuring financial stability during challenging times. For example, a professional who suffers an accident may rely on disability insurance to cover living expenses while recovering. This type of insurance is critical for individuals whose livelihoods depend on their ability to work.Travel Insurance

Travel insurance is designed to cover various risks associated with traveling, including trip cancellations, medical emergencies, and lost luggage. For instance, if a traveler has to cancel their trip due to an unexpected illness, travel insurance can reimburse non-refundable expenses. This insurance is particularly valuable for frequent travelers, as it mitigates the financial impact of unforeseen events that can occur while traveling.Importance of Choosing the Right Type of Insurance

Selecting the appropriate type of insurance is essential as it aligns coverage with individual circumstances and needs. Factors such as lifestyle, financial situation, and potential risks must be considered when choosing insurance. Individuals should assess their specific needs and seek professional advice if necessary to ensure they obtain suitable coverage that adequately protects them and their assets.Insurance Policies

Insurance policies serve as the foundational agreements between insurers and policyholders, detailing the terms under which the insurer will provide coverage and the obligations of both parties. Understanding these policies is critical for individuals and businesses to ensure they are adequately protected against potential risks. A well-structured insurance policy Artikels a broad range of components, exclusions, and benefits that can significantly affect the coverage provided.Components of a Standard Insurance Policy

A standard insurance policy consists of several key components, each contributing to the overall understanding and application of the coverage. These elements include:- Declarations Page: This section contains essential information such as policyholder details, coverage limits, and the policy period.

- Insuring Agreement: This specifies what risks are covered and under what conditions the insurer will pay claims.

- Exclusions: A detailed list of what is not covered by the policy, which is critical for understanding the limitations of coverage.

- Conditions: These are the terms and obligations that the policyholder must adhere to in order for the coverage to remain valid.

- Endorsements: Additional provisions that modify or expand the coverage, often added to tailor the policy to specific needs.

Common Exclusions in Insurance Policies

Understanding exclusions is essential as they define the boundaries of coverage and help policyholders recognize the limitations of their insurance. Below is a list of common exclusions found across various types of insurance policies:- Intentional acts or criminal behavior

- Wear and tear or gradual deterioration

- Natural disasters like floods or earthquakes (unless specifically included)

- Business activities for personal insurance policies

- Liability arising from professional services

- Acts of war or terrorism

- Property damage due to lack of maintenance

Comparison of Insurance Policy Features and Benefits

A comprehensive comparison of different insurance policies can aid consumers in selecting the right coverage based on their unique needs. The following table illustrates various features and benefits associated with different types of insurance policies:| Type of Insurance | Coverage Features | Benefits |

|---|---|---|

| Health Insurance | Inpatient and outpatient coverage, preventive services | Access to healthcare services, reduced medical expenses |

| Auto Insurance | Liability, collision, comprehensive coverage | Protection against financial loss from accidents, theft, or damage |

| Homeowners Insurance | Property coverage, liability protection, additional living expenses | Safeguards home investment, provides peace of mind |

| Life Insurance | Term and whole life options, death benefit | Financial security for dependents, potential cash value accumulation |

| Disability Insurance | Income replacement during illness or injury | Ensures financial stability during recovery |

The selection of an appropriate insurance policy involves a careful analysis of the components, exclusions, and benefits to ensure adequate protection against unforeseen risks.

Insurance Premiums

Factors Influencing Insurance Premium Rates

Numerous factors determine the rates of insurance premiums, and recognizing these can aid individuals in making informed choices. Key elements include:- Age and Gender: Younger drivers typically face higher auto insurance rates due to their inexperience, while women often benefit from lower rates in certain categories.

- Location: Premiums can vary dramatically based on one's geographical area, influenced by local crime rates, weather patterns, and population density.

- Claims History: A history of frequent claims can signal higher risk to insurers, thus leading to elevated premium costs.

- Credit Score: Many insurers incorporate credit scores into their pricing models, believing that a higher score correlates with lower risk.

- Coverage Levels: The extent of coverage selected directly impacts premiums; higher coverage limits or lower deductibles generally result in higher costs.

Methods for Reducing Insurance Premiums

Reducing insurance premiums can be achieved without sacrificing essential coverage. Implementing certain strategies can lead to significant savings:- Bundling Policies: Purchasing multiple policies from the same insurer can often lead to discounts.

- Increasing Deductibles: Opting for a higher deductible can lower premiums, but it’s crucial to ensure that the deductible remains affordable in case of a claim.

- Maintaining a Clean Record: Safe driving and minimal claims can help in securing better rates over time.

- Discount Programs: Many insurers provide discounts for various reasons, such as loyalty, professional affiliations, or completing safety courses.

- Regular Policy Reviews: Periodically reassessing coverage needs can allow policyholders to adjust their policies to avoid overpaying.

Relationship Between Deductibles and Premiums

Understanding the correlation between deductibles and premiums is vital for effective insurance management. Generally, the relationship is inverse; as deductibles increase, premiums tend to decrease. This is because:Higher deductibles mean the policyholder assumes more risk, leading insurers to offer lower premiums in exchange for that increased risk.In different types of insurance, this relationship can manifest uniquely. For instance:

- Health Insurance: Higher deductibles might lower monthly premiums, making health insurance more affordable for those who do not anticipate frequent medical visits.

- Auto Insurance: Choosing a higher deductible in auto insurance can significantly reduce premium costs, but it requires careful consideration of potential out-of-pocket expenses.

- Home Insurance: In homeowners insurance, a higher deductible may reduce premiums but could leave homeowners financially vulnerable in the event of significant damages.

Claims Process

Filing an insurance claim can often feel overwhelming, but understanding the process can simplify it significantly. The claims process is vital as it determines how and when you will receive compensation for your losses. By being informed about the steps and preparing accordingly, you can streamline your experience and enhance your chances of a successful claim.When it comes to filing an insurance claim, several general steps are typically involved. Each step plays a crucial role in ensuring that your claim is processed efficiently and accurately. The following Artikels these essential steps:Steps Involved in Filing an Insurance Claim

1. Report the Incident: As soon as the event occurs—whether it's an accident, theft, or damage—notify your insurance company. Most insurers have a 24/7 claims hotline, allowing you to report incidents promptly. 2. Document the Damage: Gather evidence of the damage or loss. This includes taking photographs, making note of the circumstances, and gathering any witness statements, if applicable. 3. Complete the Claim Form: Fill out the insurance company's claim form accurately. Provide detailed information about the incident, including dates, times, and descriptions of the damages. 4. Submit Documentation: Along with the claim form, submit all relevant documentation that supports your claim, such as receipts, police reports, or medical records. 5. Follow Up: After submission, regularly follow up with your insurer to monitor the status of your claim. Be proactive in providing any additional information they may need.Preparing Documentation to Support an Insurance Claim

Proper documentation is critical in supporting your insurance claim. The quality and completeness of your documentation can significantly impact the outcome. Consider the following tips to prepare effectively:- Keep Records Organized: Maintain a dedicated folder for all documents related to the claim. This includes the initial incident report, communication with your insurer, and any follow-up correspondence. - Collect Evidence Thoroughly: Capture clear photographs of damages or losses from multiple angles. If applicable, keep a detailed log of any expenses incurred due to the incident, like temporary housing or repairs. - Obtain Third-party Reports: If applicable, gather reports from authorities (e.g., police or fire department) that can corroborate your claim. - Include Personal Statements: Write a detailed account of the incident in your own words, emphasizing key aspects that illustrate the context and severity of the loss.Challenges Faced When Filing Claims

Filing insurance claims can present several challenges that policyholders must navigate. Common issues include delayed responses from insurers, disputes regarding the validity of claims, or disagreements over the compensation amount. To overcome these challenges, consider the following strategies:- Be Persistent: If responses are slow, don't hesitate to follow up regularly. Document each interaction with dates, names, and details discussed to track your claim's progress. - Know Your Policy: Familiarize yourself with the terms and conditions of your insurance policy. Understanding your coverage will help you better advocate for your claim and clarify any misunderstandings with your insurer. - Seek Professional Help: If you're facing significant obstacles, consider consulting a claims adjuster or an attorney specializing in insurance claims. They can provide expertise and assistance in navigating complex claims. - Keep Emotions in Check: Claims processes can be stressful and emotionally charged. Remain calm and respectful in your communications with the insurer to maintain a constructive dialogue.“Being well-prepared and informed can turn the potentially daunting claims process into a manageable task.”

FAQ Explained: Insurance

What is the difference between term and whole life insurance?

Term life insurance covers you for a specified period, while whole life insurance provides coverage for your entire life and includes a cash value component.

How can I lower my insurance premiums?

You can lower your insurance premiums by increasing deductibles, maintaining a good credit score, bundling policies, and taking advantage of discounts offered by insurers.

What should I do if my claim is denied?

If your claim is denied, review the denial letter for specifics, gather additional evidence if needed, and consider appealing the decision with your insurer.

Is insurance mandatory?

While not all insurance types are mandatory, certain types, like auto insurance in many regions, are legally required to operate a vehicle.

How often should I review my insurance policies?

It's advisable to review your insurance policies annually or after significant life events, such as marriage, buying a home, or having children.

When shopping for car insurance, it's crucial to compare auto insurance quotes from different providers. This allows you to find the best coverage at the most competitive rates, ensuring you don’t overpay for your policy while still getting the protection you need.

Understanding the landscape of insurance can be overwhelming, but knowing the best insurance companies helps simplify the decision-making process. These companies not only offer competitive rates but also provide exceptional customer service, ensuring you’re in good hands when you need to file a claim.